Cash is increasingly less important in transactions, while digital payments are increasingly widespread globally. In 2023, Global non-cash transaction volume reached $1.411 trillionand is expected to reach 1,650 billion by 2024. These are the data that emerge from the World Payments Report 2025 Of Capgeminiwhich also highlights another aspect that deserves attention: traditional credit and debit cards are losing ground to account-to-account payments.

The growth of digital payments shows no signs of slowing down

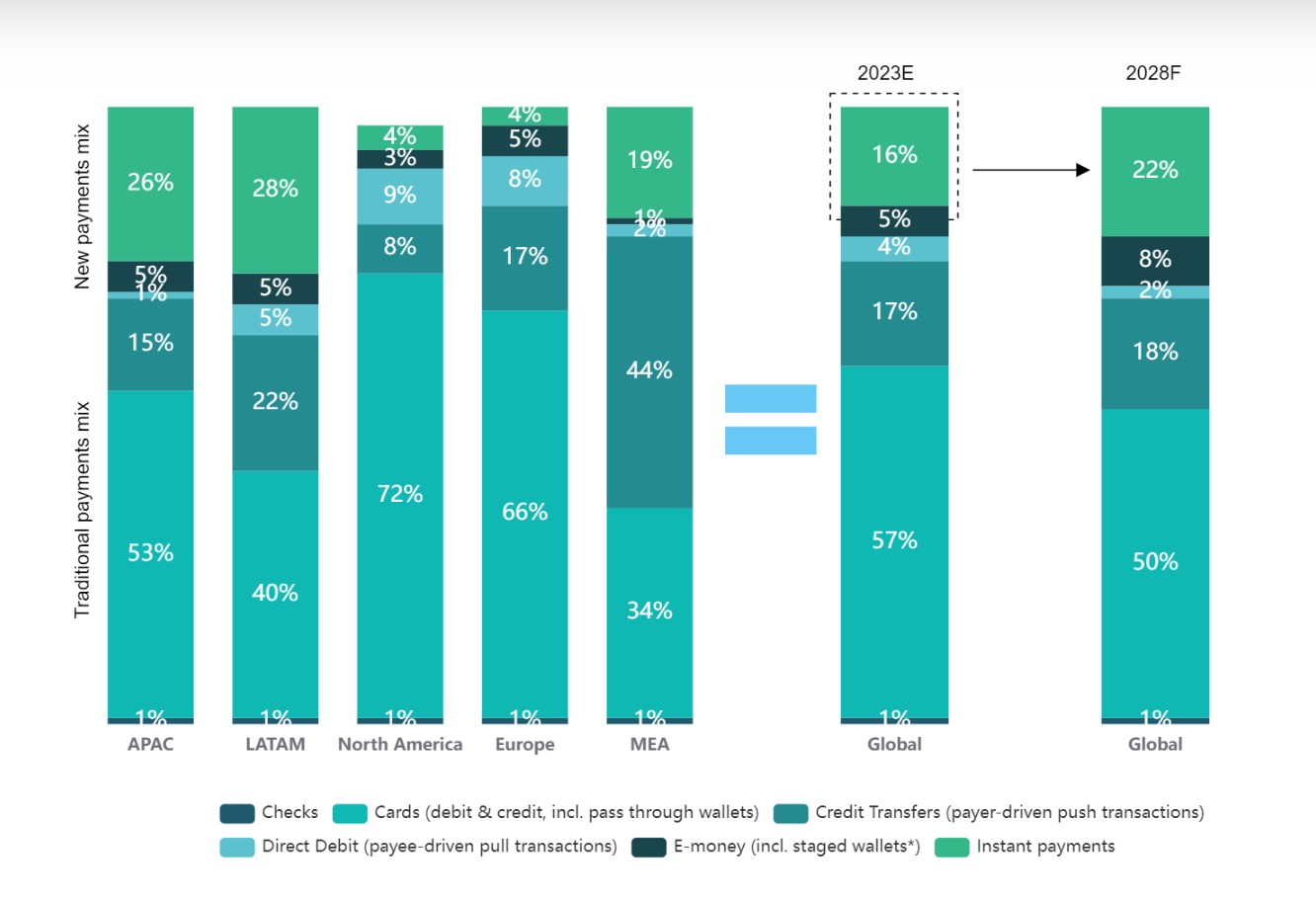

Cash is increasingly less used by people, who over time are increasingly relying on alternative solutions for payments. Following the current trend, According to Capgemini, the value of digital transactions will exceed 2.8 trillion by 2028. The area that has seen the greatest growth in the last year is APAC, with an increase of 20%, followed by Europe (16%) and North America (6%). These forms of payment are mainly driven by the growing spread of e-commerce.

Nothing new, if you look closely: for years, thanks also to the push of the new generations who prefer to do everything digitally, cash continues to lose ground compared to other forms of payment. But the Capgemini report contains an interesting fact: it is not payments with cards or apps such as PayPal that are growing the most, but sistemi account-to-account (A2A).

Today, A2A payments represent a way to quickly and safely transfer money from your current account without going through banking circuits. This is a significant advantage, since interbank commissions are avoided. In Italy, the best-known example is that of MyBank. The focus on this type of solution is overshadowing credit cards, so much so that according to estimates they could absorb between 15 and 25% of the growth in card transaction volumes in the future. A further boost to A2A payments will come, according to Capgemini, from Wero digital wallet from the European Payments Initiativewhich will accelerate adoption. 37% of European payments executives expect card transaction growth in Europe to decline significantly by 2027.

Second Dario PatriziFinancial Services Director of Capgemini in Italy, “The continued growth of non-cash transactions is a major turning point for banks and payment service providers. The data points to an inevitable shift towards a future of instant and open payments. The progress made with Pix in Brazil and UPI in India clearly demonstrates that success relies on public-private collaboration. Some financial institutions are upgrading their payment hubs or tapping into shared banking infrastructure, while consumers continue to demand instantaneity and businesses are willing to pay a premium for innovative solutions that solve their problems: it is time to create these conditions“.

Instant payments are becoming more popular, but banks are lagging behind on this front

The report shows that one way to reduce the use of cash is to accelerate the adoption of instant payments, already made available by some banks, although often at a surcharge.

However, we are talking about a rather limited percentage: Today only 25% of banks can receive instant payments, while 53% are able to send and receive them. In more detail, the report notes that only 5% of the institutes demonstrate to be highly prepared from a commercial and technological point of view and consolidate their leadership position in the adoption of instant payments. In particular, only 13% of European banks have a solid technological foundation for instant payments. This is particularly relevant for EU banks and payment service providers (PSPs), in view of the expiry of the Instant Payments Regulation (IPR) in October 2025, which requires all entities to offer full functionality for sending and receiving instant payments.

But why are banks so far behind on this front? The problem is due to security: Most bank executives say they are concerned about the risk of fraud.

Source: edge9.hwupgrade.it